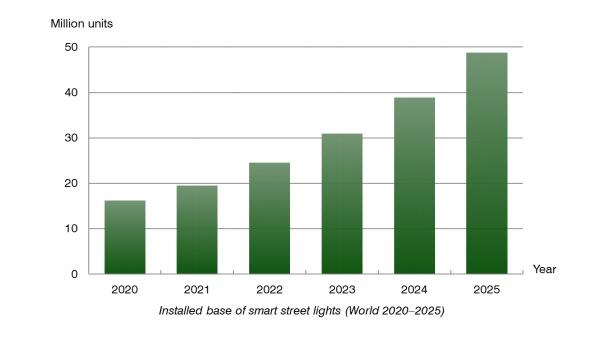

According to a new research report from the IoT analyst firm Berg Insight, the installed base of smart street lights amounted to 16.2 million globally at the end of 2020.

Growing at a compound annual growth rate (CAGR) of 24.8 percent, the installed base will reach 48.8 million by the end of 2025. Europe leads the adoption of smart street lighting technology and accounted for as much as 35 percent of the global installed base in 2020. North America continues to lag behind Europe but is nevertheless growing robustly, accounting for around 24 percent of global shipment volumes in 2020. China was at the same time home to more than half of the installed base of smart street lights outside Europe and North America, while the Rest of World region excluding China constitutes the fastest growing market.

The world’s leading smart street lighting vendor was at the end of 2020 UK-based Telensa which with nearly 2.1 million connected street lights accounted for 12.8 percent of the global installed base. Included in the top three were also Dutch Signify and US-based Sensus, of which the latter primarily serves the market through its SELC brand. In total, the top three vendors accounted for nearly a third of the global installed base of individually controlled smart street lights. Major smart street lighting players also include CIMCON Lighting, Dimonoff, Acuity Brands, LED Roadway Lighting, Current and Ubicquia from North America; Lucy Zodion and SSE from the UK; Rongwen Energy Technology Group from China; Revetec from Italy; Schréder from Belgium; Flashnet from Romania; and ST Engineering Telematics Wireless from Israel/Singapore. US-based Itron furthermore constitutes a global leader in the networking and CMS segments.

Levi Ostling, smart cities analyst, Berg Insight, said:

“The smart street lighting market continued to experience healthy growth throughout 2020 despite the Covid-19 pandemic, though the market might see a slight hick-up in its growth tempo during 2021 following some temporary delays in the issuance of tenders for new projects in the midst of the crisis.”

A number of new growth opportunities is at the same time emerging in the market. Procurements for large-scale deployments in the South American market have for example in the past two years really started to pick up pace while activity is also growing in the potentially huge Indian market.

“We have now also reached the point in time where the first large-scale replacements of early smart street lighting technology installations start to appear”, continued Mr. Ostling.

In June, Telensa became the first vendor to announce a major replacement project and a growing number of similar projects are expected to follow in early adopter markets such as the UK in the next years.